There’s no rewind on life. But you can have a practice run at retirement.

Retirement has a marketing problem. It’s sold as a long holiday: fewer emails, more golf, maybe a Wednesday that looks suspiciously like a Saturday. The reality is that retirement is not a destination. It’s a new operating system – with different income rules, different risks, and (crucially) a different you.

The biggest retirement mistakes are rarely about ‘not knowing’ – they’re about ‘not doing’.

What does it mean to ‘practice’ retirement?

What does it mean to ‘practice’ retirement?

Think of it like a fire drill. Nobody runs a fire drill because they hope for a fire. You do it because the panic is predictable, and practice makes the panic smaller. A retirement rehearsal is simply a structured trial run where you test:

- whether your budget works when the salary stops.

- whether your portfolio can survive withdrawals and market drama.

- whether your time has shape and meaning

- whether your admin (wills, beneficiaries, accounts, medical cover) is actually up to date.

whether your retirement plan survives the things life does best: surprises.

The goal isn’t perfection. It’s discovering the weak spots while you still have a payslip.

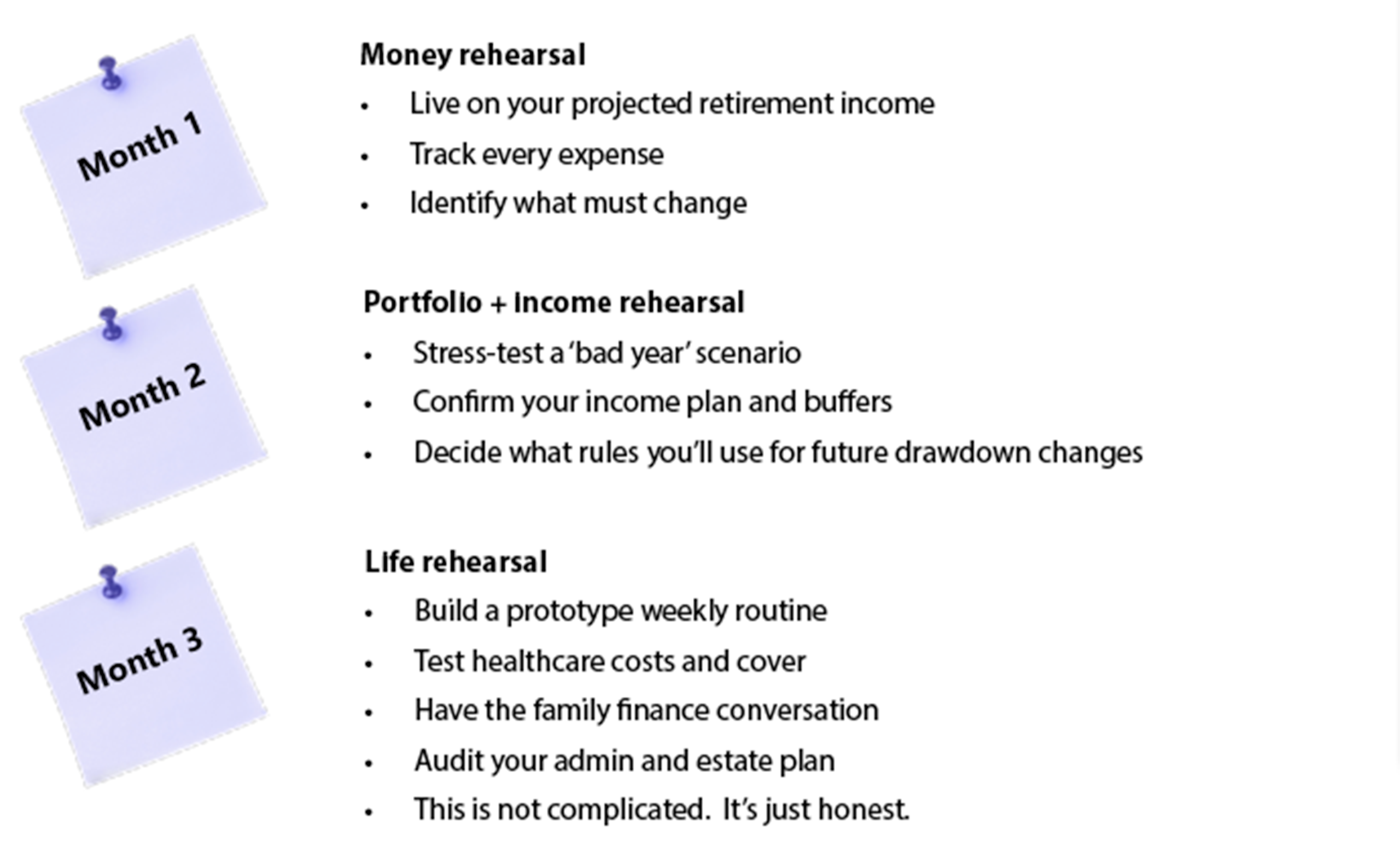

The first rehearsal: Live on your retirement income for 90 days

This is the most effective (and least glamorous) retirement planning tool available. Pick a realistic retirement income number – not the hopeful one – and live on it for three months. If your plan assumes you’ll draw, say, R40 000 a month, then for 90 days you live on R40 000. Not ‘R40 000 plus the weekend special at the Grill House, just this once-off R40 000

What happens next is always educational.

What you learn very quickly

- Which costs are fixed and unforgiving (medical aid, rates, car insurance, debt repayments).

- Which costs are quietly growing (subscriptions, takeaways, family support, ‘little’ lifestyle creep).

- Which costs you forgot entirely (home maintenance, car replacement, travel to see family, tax surprises).

The ‘win’ if it goes well. If you can comfortably live on your projected income, you’ve just bought yourself something priceless – confidence.

The ‘win’ if it goes badly. f it doesn’t work, you’ve discovered it early enough to do something about it: save more, work longer, reduce debt, adjust expectations, restructure income. Either outcome is progress.

The second rehearsal: Practice withdrawals, not just returns

Most people plan retirement as if markets behave politely. They don’t. The single most underestimated risk in retirement isn’t volatility. It’s volatility + withdrawals at the wrong time, especially early on. If you draw income while the portfolio is down, you can permanently damage the engine that’s meant to power the next 25 – 35 years.

So, in your rehearsal, don’t just ask ‘What return might I get?’ Ask ‘What happens if I need income during a bad year?’ A practical way to do this: build income ‘shock absorbers’. A sensible retirement structure usually needs at least some combination of:

- A cash buffer (so you’re not forced to sell growth assets at a bad time)

- A bond/income allocation (more stable, less exciting, the buffer between cash and your growth assets)

- A growth portfolio (equities, local and offshore (hedging our bets regarding the rand)

- A rules-based drawdown plan (so that both the planned for income and the emergency funds are deliberate, not emotional)

- You can call it a ’bucket strategy’ if you like. Or you can call it ‘not panicking in public’.

The third rehearsal: Practice your time – because boredom is expensive

Nobody warns you that retirement can be oddly… noisy. Not externally. Internally.

Work gives you structure, social contact, identity, and a reason to put on shoes. Remove that, and many retirees default into two traps:

- Spending to fill the gap (‘Let’s go away again…’).

- Drifting through unstructured days (because too much empty time can turn into anxiety)

So, part of retirement rehearsal is testing your week.

Build a prototype week

- 2-3 anchors (exercise, volunteering, a hobby with other humans, a part-time gig, mentoring)

- a ‘social rhythm’ (friends don’t magically appear because you’re free at 10am) so join a ‘line-dancing’ group or play bridge once a week. Set up coffee dates, or grandchildren visits etc.

- a purpose project (something you build, teach, grow, coach, create)

Retirement works best when leisure is planned for, not when it just happens.

The fourth rehearsal: Practice healthcare costs like you mean it

In South Africa, healthcare inflation has no respect for your spreadsheet. Medical aid is often the single biggest line item that rises relentlessly in retirement. And then there’s gap cover, chronic medication, dentistry, hearing aids, unexpected procedures, and the small matter of living long enough for all of this to matter.

A retirement rehearsal should include:

- reviewing medical aid options before you retire (when affordability still has levers).

- modelling ‘bad luck’ years, not just average years.

- checking whether your plan assumes you’ll downgrade cover later (many people say they will; few do).

- This is one of those areas where optimism is not a strategy.

The fifth rehearsal: Practice ‘family finance boundaries’

Retirement planning often collapses under one sentence ‘We’re helping the kids for a bit.’ In South Africa, that ‘bit’ can become a decade. Adult children living at home longer, extended education timelines, first-home deposits, weddings, and sometimes grandchildren’s school fees – all noble, all human, all capable of quietly detonating retirement maths.

If you want your retirement to work, generosity needs a policy, not a mood.

A practical approach

- Agree on limits, timelines, and what you will and won’t fund.

- Separate ‘support’ from ‘subsidy’.

- Put it in writing if needed (because you’re serious).

The harsh truth – you can borrow for a child’s education (in theory). You cannot borrow for your own old age.

The sixth rehearsal: Practice the admin that nobody wants to talk about

Retirement is when paperwork stops being annoying and starts being decisive. Before retirement, do a full ‘admin audit’

- beneficiaries on retirement products and life cover

- up-to-date will/s

- executor arrangements and where documents live

- passwords and digital access for your spouse/executor

- what happens to income products on death (especially where nominations matter)

If you’re using living annuities, preservation funds, retirement annuities, or a combination, you want complete clarity on what sits inside the estate and what sits outside it – because they don’t follow the same rules.

The seventh rehearsal: Practice location decisions, not just lifestyle fantasies

‘Let’s retire at the coast’ is a sentence that has bankrupted more people than they’ll admit. Sometimes it works brilliantly. Sometimes it becomes:

- higher municipal costs than expected

- services that don’t match the brochure

- a house that eats maintenance money

- distance from family and healthcare networks

- property illiquidity at the exact moment you want flexibility

A retirement rehearsal can include doing a trial stay (weeks, not days) and costing it properly – including running costs and travel back to your support network. Romanticising retirement towns is easy. Living in them is the test.

A simple retirement rehearsal plan (that you can actually execute)

If you want a practical checklist, here’s one that works:

The uncomfortable conclusion (and it’s a useful one)

If you’re avoiding rehearsing retirement, it’s often because you’re afraid of what you’ll learn. But what you learn is exactly what gives you power. If the rehearsal shows you’re on track, you retire with confidence.

If the rehearsal shows gaps, you still have time – and time is the most valuable retirement asset you’ll ever own.