The first place to draw money from in retirement (and why many of us get it backwards)

There’s a moment that arrives for many South Africans in their late 50’s or 60’s when the conversation shifts. You stop talking about what you are busy buying and start talking about what you are going to use. The vocabulary changes: ‘growth’ becomes ‘income’, ‘long term’ becomes ‘this month’, and suddenly you find yourself staring at a question that feels oddly basic for something you’ve spent decades building:

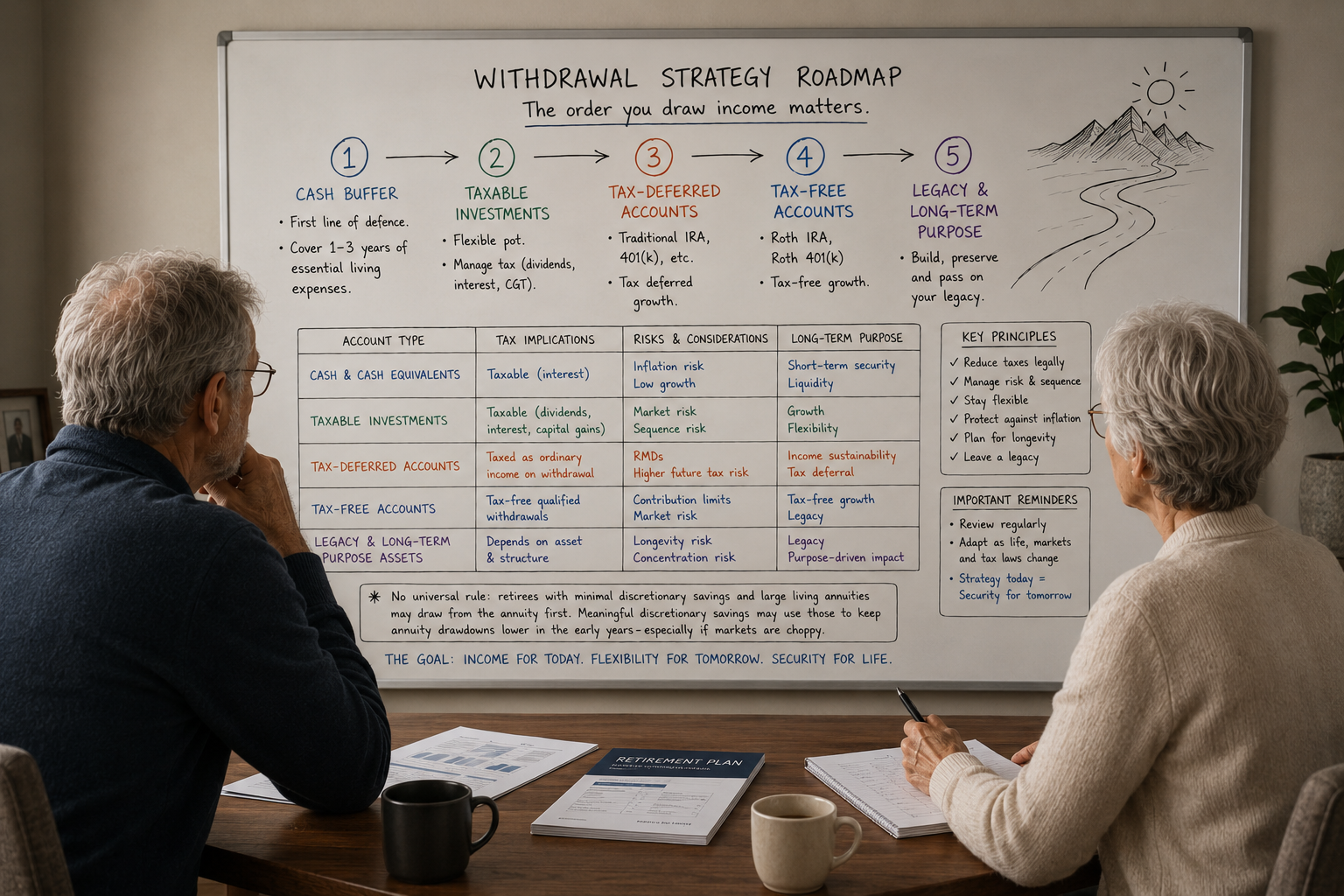

Where do I take the money from first?

It’s a deceptively simple – though very important – question, and the culmination of the first half of one’s retirement plan – the savings phase. Any portfolio of long-term savings has multiple ‘pots’ of money, and the order in which you tap into them can meaningfully affect tax, flexibility, investment performance, risk profiling, and how long your capital lasts.

Before triggering the first income withdrawals from one’s portfolio, several considerations are required. Any income withdrawal (and of course this will now be ongoing) requires cognisance of the tax consequences, regulatory constraints, and a clear understanding of the differences between the various asset classes.

Here we’ve segmented assets based on them being defined as one of: growth, income producing, capital preserving, or speculative. Ensuring the portfolio continues to be managed within a defined ‘plan’ needs election of which assets are sold to provide the income retirement demands. And then of course you also need to allow enough slack for the odd curve-ball which will almost certainly be thrown.

Retirement isn’t for sissies…

While this asset election process can be planned for, it’s never just a paint-by-numbers undertaking. There’s no universal sequence that works for everyone. The point is to give you a practical way to think about the order of withdrawals – and how to avoid accidentally pulling from the ‘wrong’ place first.

The quiet mistake: Treating all money as the same money

If you’re still earning a salary, your financial life tends to behave like a simple river: income flows in, expenses flow out, investments sit on the side growing quietly (or loudly, depending on the year).

Retirement is different. Retirement is more like having several taps in your kitchen, all connected to different pipes, with different pressures, and different municipal bylaws. One tap is taxable. One tap is tax-free. One tap comes with penalties if you use it too early. One tap is technically allowed to gush at 17.5% a year, but that doesn’t mean it should.

The first error many retirees make is emotional: they assume the ‘best’ pot is the one that feels safest. Usually that means cash. There’s comfort in seeing money sitting still. You can touch it.

The problem is that cash has a hobby: it quietly loses value to inflation. And then there are the tax consequences. So yes, cash is useful. But too much cash is not conservative – it ’s actually expensive. Cash should be your shock absorber.

Step one: Cash

Step one: Cash

If you’re retiring (or newly retired), one of the smartest things you can do is keep a deliberate cash buffer – money that exists to fund short-term spending and protect you from having to sell long-term investments at a bad time, when markets are misbehaving.

That’s particularly important if you’re using a living annuity and your investment markets decide to have a tantrum right when you begin drawing an income.

So, start with cash in the sense of: ‘I’m drawing from my buffer while I give my longer-term investments time to behave.’

But here’s the discipline: cash should be sized, planned, and replenished when conditions allow – not treated like a mattress you never disturb. Long-term cash isn’t a buffer; it’s a slow leak.

Step two: Taxable investments – the ‘flexible’ pot that needs a tax brain

After cash, taxable accounts, or discretionary savings, are the next logical source -on the basis that they are generally less tax-efficient than retirement accounts.

Unit trusts, share portfolios, endowments, and any investment outside retirement wrappers are included in this step.

This is the pot that looks easy to use, because it’s accessible. And that’s exactly why it’s dangerous to use without thinking.

The subtle advantage of taxable investments is flexibility. You can often choose what to sell (and therefore whether you’re crystallising capital gains), and you can manage withdrawals to stay within certain tax thresholds. You can also ‘manage’ your CGT.

For many retirees, drawing from discretionary taxable investments early on can make sense because it gives your retirement products more time to compound, while you keep greater control over tax outcomes. This assumes adequate savings. It may be that drawing from a living annuity is a necessity and not a choice.

The takeaway: Taxable investments are flexible, but they are not ‘free’. They require a tax-aware withdrawal plan, not guesswork.

A quick detour: The temptation to fund retirement by selling ‘stuff’

A quick detour: The temptation to fund retirement by selling ‘stuff’

There’s nothing wrong with using real assets as part of retirement funding – provided you treat them for what they are – illiquid, sometimes emotionally loaded, and often subject to unpredictable pricing. The weekend cottage or the MGA fall into this category. Markets and buyers may not coincide with your disposal. Treat real assets as options, not as the only exit door.

The South African curve-ball: The tax-free savings account is not a magical ATM

Now we get to the pot that South Africans love – the tax-free investment (TFSA). So why not draw from it early in retirement, if it’s ‘tax-free’? Because the TFSA has a sting in the tail: when you withdraw and later put money back, that reinvestment counts as a new contribution and affects your annual and lifetime limits. That means the TFSA is not just a tax wrapper – it’s a scarce tax wrapper.

So, for many retirees, the TFSA is best treated like the last bottle of water on a hot road trip. Often, the TFSA is the most valuable long-term compounding tool in a family’s financial system – and one of the best legacy assets you can leave behind precisely because of its tax efficiency.

Retirement funds and living annuities: The pot that looks stable… until it isn’t

Most South Africans don’t retire with one neat investment account. They retire with a combination of retirement funds (pension, provident, RA, preservation funds) and then a retirement income product such as a living annuity or guaranteed annuity.

A living annuity is wonderfully flexible – you choose your drawdown rate within regulated limits. But those limits are wide: 2.5% to 17.5%. Try and keep drawings below the portfolio’s annual performance.

Once you are drawing from a living annuity, you are effectively running a long-term project: managing market risk, longevity risk, and your own behavioural risk. If you draw too much early on – especially after a bad market year – you can do permanent damage to the sustainability of the income.

Where flexibility exists, it can make sense to use other assets tactically to avoid excessive annuity drawdowns during volatile periods. And if you have a guaranteed annuity component (or other stable income), you may have created something very useful: an income floor that allows you to keep the living annuity invested for long-term growth without panicking.

So, what’s the practical answer?

The best withdrawal order is the one that keeps you liquid, tax-aware, and psychologically calm. This should all happen whilst giving your best compounding assets time to do their job, typically starting with cash and then taxable accounts before tax-advantaged accounts. You’d adapt it roughly like this:

- You begin with a cash buffer that has a purpose.

- Then you look to flexible discretionary investments, but you do it with tax awareness.

- You treat the TFSA with respect because it’s scarce and powerful, and SARS effectively punishes sloppy use of contribution room.

- You manage living annuity drawdowns carefully because the rules allow you to draw too much long before they stop you.

- And you remain open to using ‘big asset’ sales as part of the plan – but not the plan.

The real conclusion: Retirement withdrawals are a strategy, not a transaction

If you take only one thing form this article let it be this: retirement doesn’t only require a good investment strategy. It requires a good withdrawal strategy.

Withdrawal strategy is about avoiding seemingly reasonable short-term decisions that create long-term damage.

Which pot will you draw from in a normal year? What changes in a bad market year? Which pot is protected for later life? Which pot is meant for flexibility? Which pot is meant for legacy? And what is the maximum drawdown that still allows you to sleep at night?

Retirement is supposed to buy you freedom. The irony is that the right withdrawal order often gives you that freedom by doing something very unglamorous: putting some rules in place while you’re still thinking clearly.