Market Overview – Third quarter 2025

Market commentary

-

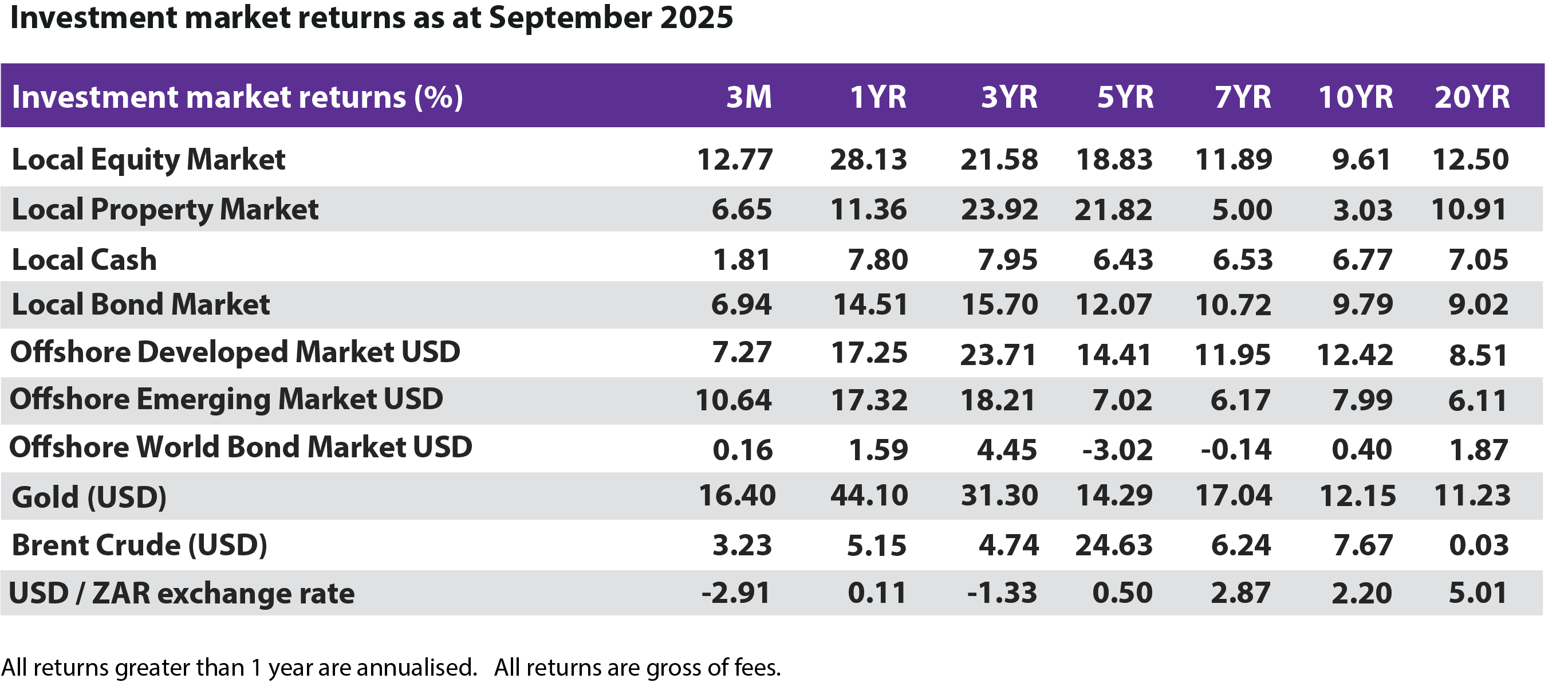

Local equities ended the quarter some +12.8% up, primarily driven by the +50.8% Resources sector gain. The Industrials sector added +3.7%, Listed Property +6.7% and Financials +0.9%. Gold and Platinum counters have gained double to triple digit returns over the year as the underlying commodity price continues to run amid global demand. SA Inc. (companies whose earnings are overwhelmingly linked to our own economy) has struggled over the year as investors have preferred mining companies. The broader SA equity market outside of the top ten performing stocks have nonetheless yielded positive single digit returns over the year.

-

The South African economy grew by some +0.8% quarter-on-quarter in Q2 2025, improving on the +0.1% growth in Q1 and beating forecasts of +0.5%. The South African Reserve Bank (SARB) cut interest rates by 0.25% in July but kept rates unchanged at 7% in September, citing a drive towards the lower inflation target and signaling caution amid global uncertainty.

-

Local Bonds returned +6.9% for the quarter, ahead of Local Cash which earned +1.8%. Foreigner’s demand for SA Bonds continued to rise over the quarter with an aggregate R77 billion inflow in September. In part this has added some strength to the rand.

-

The MSCI Emerging Markets Index added +10.6% USD for the quarter ahead of its developed market counterpart. China’s anti-involution policy which aims to restore profitability, improve product quality, and manage overcapacity positively impacted market sentiment. Taiwan’s market outperformed the broader index due to ongoing strength in technology stocks, driven by continued demand towards artificial intelligence. Similarly, Korea’s outperformance was supported by the technology sector, particularly memory semiconductor-related companies.

-

The MSCI World Index returned +7.3% USD for the quarter. The US economy grew at a strong +3.8% annualised in the second quarter following a contraction in Q1.

-

The US Federal Reserve lowered interest rates by 25 basis points to 4.25%, the first rate cut of the year, citing slower job growth and a rising risk of unemployment. The Bank of England kept its rates unchanged in September and announced that it would cut down on its quantitative tightening programme, a move that could help reduce bond yields and borrowing costs. European Central Bank (ECB) also kept their rates unchanged in July and September. The ECB President Christine Lagarde acknowledged that the significant inflation spike experienced between 2022 and 2024 has subsided, and inflation risks are currently balanced. September’s 2.2% inflation print largely aligned with the ECB’s 2% target.

-

The price of Gold continued its upward rally +16.4% closing the quarter $3873/oz and Silver +30.1% at $46.64/oz. The rand remained stable with the dollar weakening some -2.6% against the rand over the quarter.

Whilst short-term challenges remain on the horizon, the longer-term picture remains positive. Aligned with previous communications, GTC maintains that patience through periods of uncertainty, affords markets the time needed to filter out the noise from that which is relevant. This same patience then allows market drivers and investment portfolios the required time to achieve a new state of normalcy, and commensurate compound growth.

GTC’s portfolios have been well-positioned to capitalise on the recent robust performance of both local and international equity and bond markets. While favourable, we acknowledge that the +32% return from local equities (year to date) likely represents a mean reversion from previous periods of under performance and exceeds typical long-term expectations which we caution against.

Consequently, a phase of more subdued short-term returns could reasonably follow as part of normal market fluctuations. GTC is therefore maintaining a cautiously optimistic approach to portfolio positioning as we navigate the current market environment.