Market Overview – Fourth quarter 2024

In-depth market commentary – making sense of a shifting landscape

Over the quarter:

-

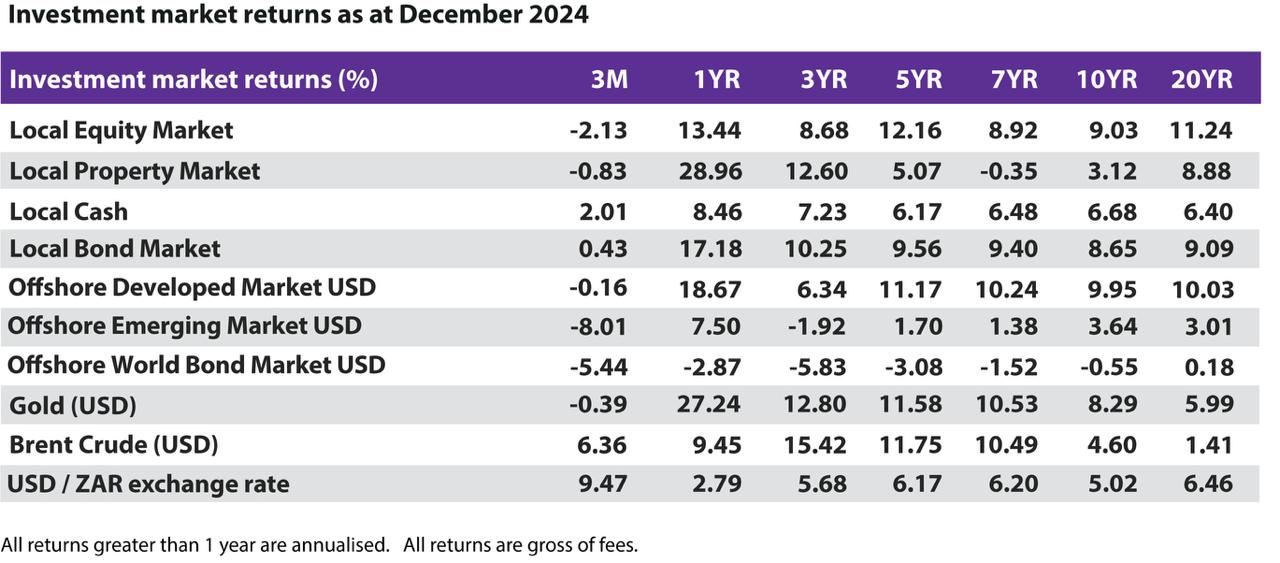

Local equities ended the quarter -2.14% in the red pulling down the 2024 full-year return to +13.4%. The Financials sector declined -1.8%, while Industrials posted a modest gain of +0.2% over the 3 months. The Resources sector was the largest detractor, down -10.1% over the quarter and -7.2% over the year. The local property sector shed -0.8% for the quarter, though its performance for the year remained strong at +29.0%, making it the best-performing local asset class of the year.

-

The South African Reserve Bank (SARB) continued its rate-cutting cycle during the quarter, reducing the repo rate by 25 basis points to 7.75%, a move that was largely in line with market expectations. The South African Chamber of Commerce and Industry (SACCI) Business Confidence Index (BCI) rose to 118.1 in November 2024, its highest level since October 2015, up from 114.2 in October.

-

Local bonds delivered a positive return of +0.4% for the quarter but lagged local cash, which achieved a return of +2.0%. Over the full year, local bonds gained +17.2% with local cash up +8.5%.

-

The MSCI Emerging Market equity index shed -8.0% USD over the quarter and gained +7.5% USD over the full year, underperforming its developed market counterpart.

-

China’s performance was negatively affected by the absence of further policy stimulus and investor concerns around the impact of proposed Trump trade tariffs. Brazilian shares were the weakest among emerging markets, as their local currency depreciated due to growing concerns over the country’s fiscal outlook. South Korea also posted losses amid political instability, with both the president and the acting president being impeached over December.

-

The MSCI World Index was mostly flat at -0.2% for the quarter, however earned +18.7% USD over the full year. The index’s positive performed is almost entirely driven by the US equity market which gained +25.0% USD.

-

The U.S. Federal Reserve cut their interest rate by a further 25 basis points in both November and December taking US interest rates to a range of 4.25% – 4.5%. Federal Reserve Chair Jerome Powell emphasised that further rate cuts would depend on progress in reducing persistently high inflation. The European Central Bank (ECB) also cut interest rates by 25 basis points in both October and December taking its interest rate to 3.15%. ECB President Christine Lagarde signalled that more rate cuts could be expected in 2025.

-

The price of Gold ended the year at $2 624 an ounce, up +27.2% amid continued demand for the commodity by central banks seeking to de-dollarise, as well as by safe-haven asset seekers. Subdued global demand prospects along with increased global supply kept the price of Brent Crude oil benign for most of the year with a +6.4% spike over the final quarter. The greenback (US Dollar) continued to weaken against the rand over the first three quarters of the year before surging +9.5% in the last quarter.

Overall, the year 2024 brought about significant turbulence driven by a series of events, each contributing to a challenging and volatile investment landscape:

-

Japan ends negative interest rates: The Bank of Japan raised interest rates, ending its 17-year negative rate policy. This triggered a sharp yen appreciation, disrupted carry trades, and caused a global sell-off in risk assets, including a swift and steep equity market pull-back in August.

-

Wall street crash: The August sell-off, reminiscent of Black Monday 1987, saw significant declines in major stock indices globally. The Yen’s appreciation and unwinding carry trades were major contributors. The overall Nikkei equity index and U.S. Tech giants were particularly hard hit, with companies like Nvidia, Apple, and Amazon losing billions in market value.

-

China’s stimulus: Unprecedented stimulus package announced late in September led to market optimism about forthcoming global growth and pushed the MSCI China Equity index up some +20% USD over the week.

-

Fed’s first rate cut: The Federal Reserve cut interest rates for the first time since the pandemic recovery. While initially welcomed, concerns about economic weakness and uncertainty about the Fed’s long-term policy direction led to market volatility.

We enter 2025 with the global investment market as interconnected as ever. President Donald Trump’s, return to the White House and his radical stance on cross-border trade has the potential to send seismic waves across the global investment landscape. While there is much uncertainty, GTC Asset Management believes that the US tariffs are in part being employed as a negotiating tool to achieve non-trade-related objectives in areas such as immigration and opioid abuse. What is certain is that this path has and will continue to rattle investor sentiment and increase doubt around implied forward-looking projections. The implementation of tariffs – to the extent that he has promised – will likely impede global trade, increase global inflation, and push central banks to re-assess their plans to further cut interest rates.

Without throwing caution to the wind, we are optimistic about global investment markets for 2025 and what they mean for our investment solutions. Short-term chaos is no stranger to investment markets, remaining white noise in the grander scheme of conventional market cycles.