Market Overview – Fourth quarter 2023

In-depth market commentary – Navigating choppy waters in the global investment arena

The year ending December 2023 has continued to reflect a challenging global investment market backdrop. Enduring economic uncertainty has prolonged elevated investment market volatility. Subdued global trade and stubborn core inflation have led to persistently restrictive monetary policies from global central banks which, with the elevated yields have prevented markets from being kept on an even footing. These heightened risk factors necessitate continued caution in portfolio positioning.

Over the quarter:

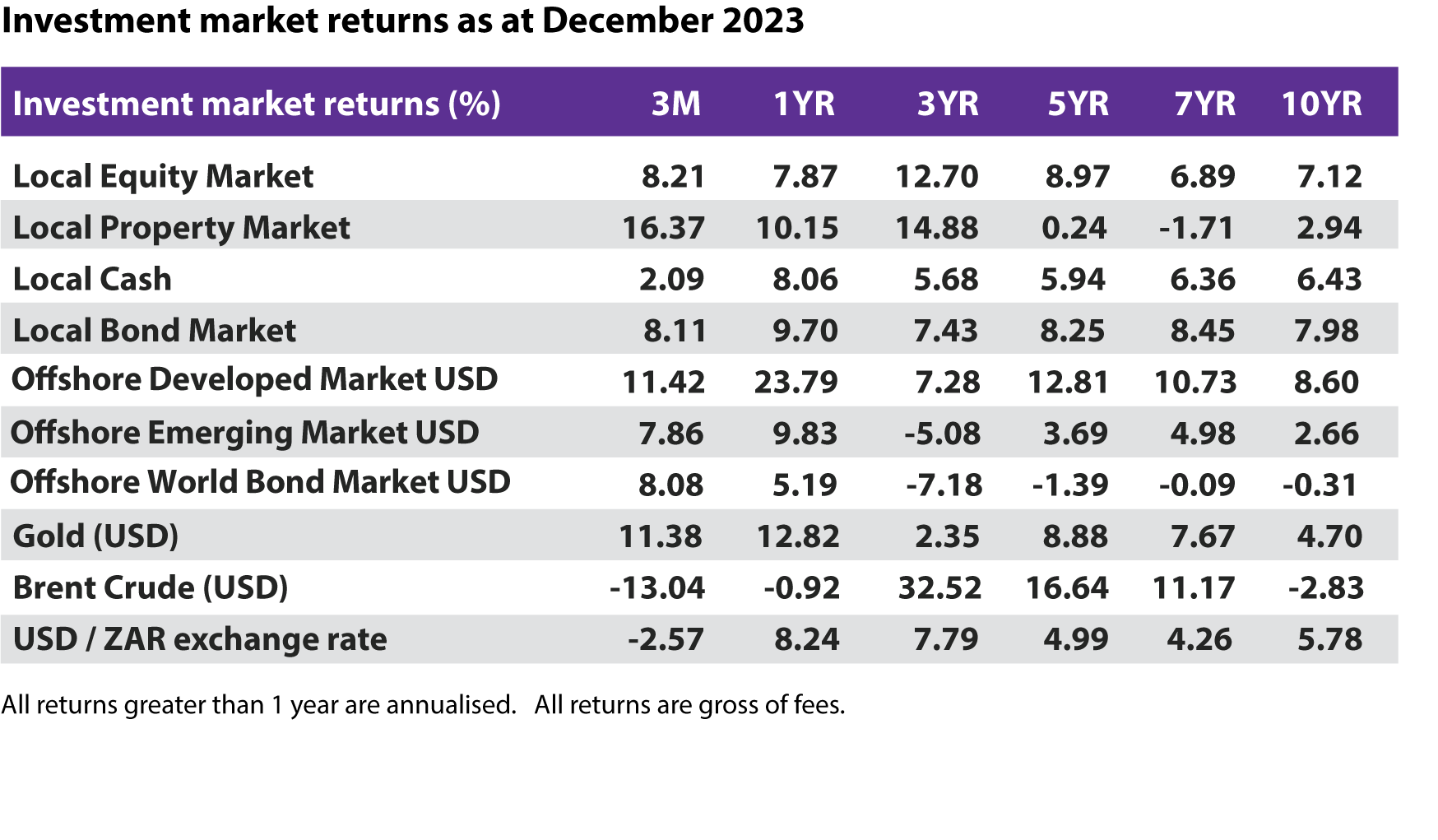

- Global developed market equities rallied +11.4% over the quarter and +23.8% over the year, well ahead of emerging market equities which delivered +7.9% and +9.8% respectively in US dollar terms. Positive sentiment around sooner-than-expected interest rate cuts from the US FED spurred investor optimism over the last quarter. The strong returns earned by both counters over the calendar year helped offset some of the impact from their sell-off during 2022. The dollar’s -2.6% weakness relative to the rand, detracted from offshore assets’ rand-based return over the quarter but added +7.8% to their return over the year.

- Local equities earned +8.2% over the three months and +7.8% over the calendar year. The quarter’s performance was primarily attributed to a strong rally in the local financials sector (+12.3%) and listed property sector (+16.4%) amid strong earnings and a slightly improved global outlook. Industrials were up (+5.9%) while the Resource sector came in flat (-0.0%) for the quarter as softer precious metal prices persisted.

- The South African Reserve Bank (SARB) kept interest rates unchanged at +8.25% as headline inflation (CPI) fluctuated, ending the quarter at +5.5%. This represents an overall +1.25% interest rate hike since the start of 2023 in their efforts to reduce inflation.

- The US FED and European Central Bank (ECB) kept interest rates unchanged. The FED increased interest rates by a total of +1.0% to +5.5% over the calendar year while the ECB increased rates by a total of +2.0% to +4.5%. Headline inflation for the year ending November 2023 came in at +3.1% for the US and 2.4% for the Eurozone.

- The local bond market (ALBI) delivered +8.1% for the quarter and +9.7% over the year ahead of local cash (STEFI) at +2.1% and +8.1% respectively. The Global Government Bond Index (WIGBI) earned +8.1% over the quarter as yields retreated.

- The Gold price breached $2 000/ounce during the year to deliver an +12.8% overall gain. Amid global growth uncertainty and production cuts by OPEC, the Brent Crude price was relatively volatile over the year to end the year at $77.0.

- Overall, global investor sentiment was mixed over the quarter. While the short-term outlook is still unclear, the longer-term picture remains positive.

The global investment market environment has been volatile over the past few years. However, patience, especially through periods of difficult investment performances, affords markets the time needed to filter out what is relevant from the noise. This same patience then allows market drivers and investment portfolios the required time to achieve a new state of normalcy, and commensurate compound growth.

The investment road is almost always a bumpy one. GTC’s solutions hedge out much of the inherent investment risk while still positioning portfolios for the highest probability of delivering on stated investment objectives. It is crucial to stay invested in line with one’s originally determined objectives. Resisting the temptation to be swayed by short-term sentiment is a permanent challenge.