Market Overview – First quarter 2025

In-depth market commentary

Over the quarter:

-

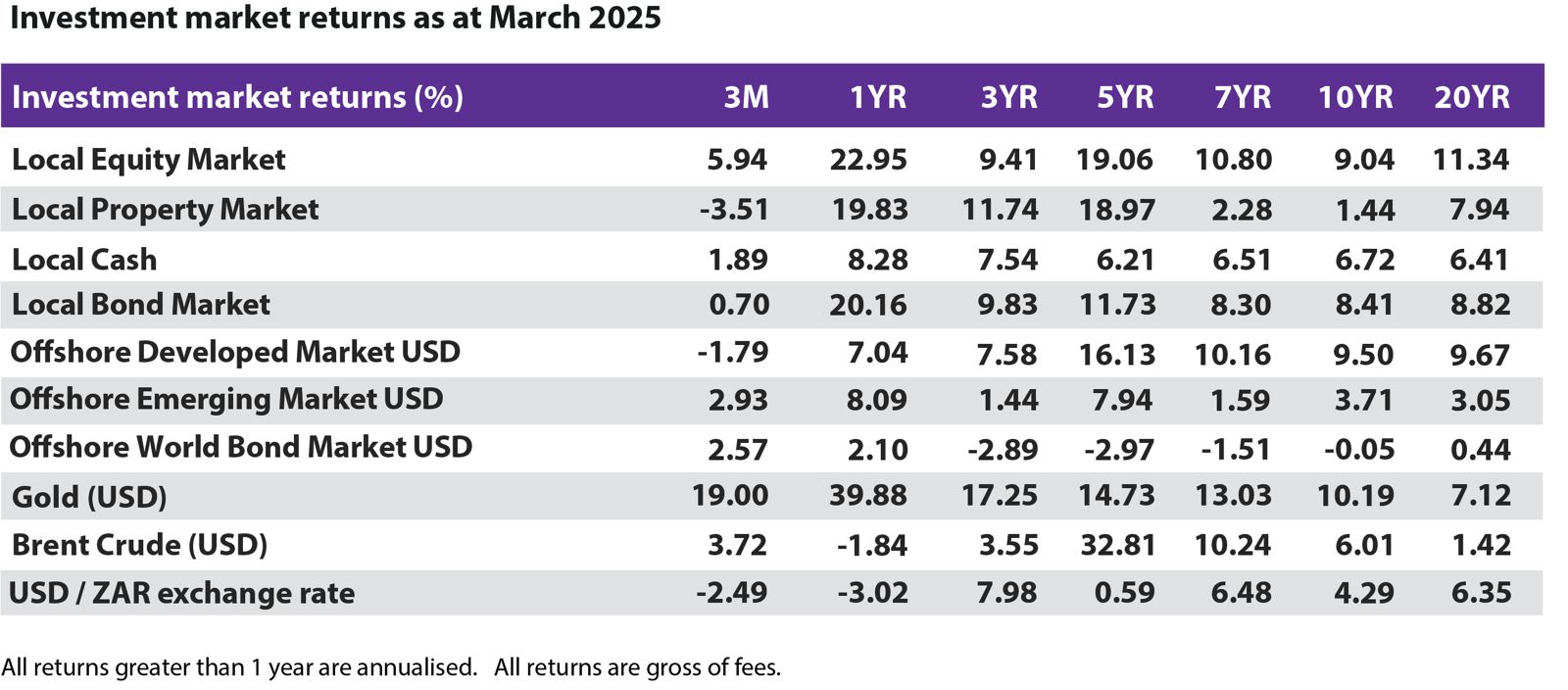

Local equities ended the quarter up +5.9%, with the Resources sector leading the rally as it gained +33.7%. The Financials sector shed -1.7% on profit taking, while Industrials sector, driven by a run in Richemont and Prosus, added +3.1%% over the quarter. The local property sector detracted -3.5%.

-

South Africa’s economy expanded 0.6% in the fourth quarter, supported by a rebound in agricultural output. In March, the South African Reserve Bank kept the repo rate unchanged at 7.50% with a cautious outlook amid the current tumultuous global environment. SA inflation ended the quarter at 3.2%, within the Reserve Bank’s target range. Subdued domestic demand coupled with a deteriorating global trade outlook, could see local inflation cool even further.

-

Local Cash yielded a return of +1.9%, outperforming local Bonds which delivered a +0.7% gain. The risk-off sentiment stemming from global trade uncertainty and domestic political tension led to decreased demand for local bonds and a subsequent increase in yields.

-

The MSCI Emerging Market equity index gained +2.9% USD, outperforming its developed market counterpart. The introduction of China’s DeepSeek, a cost-effective open-source AI model, influenced market sentiment as investors reassessed the valuation of US-based AI companies. The Caixin China General Manufacturing PMI indicated improved conditions in the manufacturing sector, rising further above the 50-point mark. This, coupled with optimism from additional Chinese government stimulus, bolstered market sentiment and contributed to a +9.2% USD return in the Chinese equity market over the quarter. India’s equity market experienced a decline of -2.9% USD due to profit-taking and some concerns regarding economic growth, which prompted the first Indian repo rate cut since May 2020, bringing their rate to 6.25%. In Brazil, inflation remained above the central bank’s target, resulting in three policy rate increases.

-

The MSCI World equity Index declined -1.8% USD for the quarter as US mega cap technology stocks turned negative. The US equity market declined -4.3% USD while global developed markets outside of the US expanded +6.2% USD over the quarter. Global risk appetite further diminished towards the end of the quarter amid anticipation of an escalation to the tariff war initiated by the US. The consequential market reaction to these tariffs have already been detailed in the GTC Market Update distributed on 10 April 2025.

-

In their respective March meetings, both the US Federal Reserve and Bank of England kept interest rates unchanged at 4.5%, maintaining a wait-and-see approach amid persistent inflation and global economic uncertainty. Meanwhile, the European Central Bank (ECB) cut its three key interest rates by 25 basis points, bringing the deposit facility rate to 2.50%. The ECB President Christine Lagarde noted that the highly uncertain macro environment complicates monetary policy decisions, diverging from her past stance suggesting a that the path is to lower rates.

-

The price of Gold concluded the quarter at $3123 per ounce, representing a 19.0% increase. This appreciation was driven by sustained demand from central banks seeking to diversify away from the USD, as well as from investors seeking safe-haven assets. The USD weakened by 2.5% against the South African rand during the quarter.

Short term chaos is no stranger to investment markets, however, this remains white noise in the grander scheme of the normal market cycle. GTC continues its portfolio construction designed to hedge out investment risk while positioning the portfolios for stated investment objectives.