A tale of two inflation rates

Inflation has become surprisingly polite. Stats SA’s latest data places headline CPI at 3.1% year-on-year to March 2026, comfortably within the South African Reserve Bank’s target range and well below the levels households endured only a few years ago. Food inflation has moderated, several staple categories have shown limited price pressure, and transport inflation remained in deflationary territory through March.

At face value, the environment appears relatively stable. Yet South African households have entered the second quarter of 2026 facing a very different lived reality, particularly after the extraordinary fuel price adjustments introduced in April and again in May. From 1 April 2026, inland petrol prices increased sharply, while diesel recorded one of the steepest monthly increases in recent history. By May, inland 95 unleaded petrol had moved above R26 per litre, with diesel climbing above R32 per litre in parts of the country.

At face value, the environment appears relatively stable. Yet South African households have entered the second quarter of 2026 facing a very different lived reality, particularly after the extraordinary fuel price adjustments introduced in April and again in May. From 1 April 2026, inland petrol prices increased sharply, while diesel recorded one of the steepest monthly increases in recent history. By May, inland 95 unleaded petrol had moved above R26 per litre, with diesel climbing above R32 per litre in parts of the country.

Fuel rarely remains a transport story for long. Higher fuel prices move quickly through logistics, food distribution, commuting costs, school transport, municipal services and broader operating expenses throughout the economy. Even where headline inflation initially appears contained, sustained fuel increases tend to filter steadily through household expenditure over subsequent months.

Which means the conversation around inflation has become considerably more complicated than the headline CPI number suggests. Because for many South African households, the real pressure point sits in the widening gap between income growth and the long-term costs shaping everyday life.

The real inflation rate

The education component of CPI is updated annually, and the latest figures continue a familiar pattern. Education inflation accelerated to 5.4% in 2026, while primary and secondary education increased by 6.2%. Private secondary schools recorded the sharpest rise at 7.5%, materially ahead of headline inflation and comfortably above the average salary increases seen across much of the economy.

Over time, this distinction becomes meaningful. A once-off increase is manageable. A persistent annual increase that compounded over more than a decade gradually reshaped household cash flow in ways that are often underestimated at the outset.

The challenge for many households is that school fees do not exist in isolation. They form part of a broader collection of structural lifestyle costs that continue to rise steadily over time, often materially ahead of CPI.

The challenge for many households is that school fees do not exist in isolation. They form part of a broader collection of structural lifestyle costs that continue to rise steadily over time, often materially ahead of CPI.

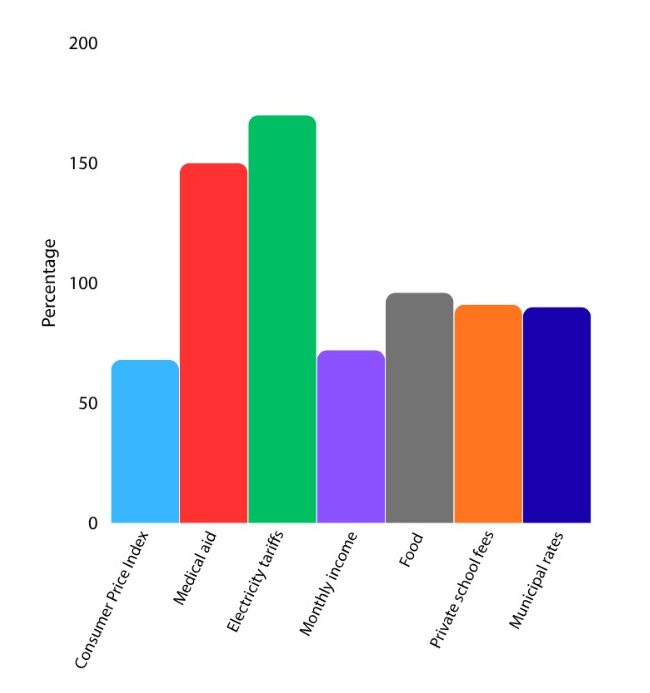

Medical aid behaves similarly. Healthcare inflation has historically exceeded headline inflation for prolonged periods, driven by specialist’s costs, hospital tariffs and utilisation trends. Municipal charges increasingly belong in the same category, particularly as electricity, rates and service-related expenses continue to rise faster than many households’ incomes. Education inflation continues to outpace headline CPI in South Africa.

The pressure building beneath the averages

Headline CPI is designed to reflect a broad basket of goods and services, combining everything from food and transport to housing, communication and recreation into a single national number. The difficulty is that these categories move differently and affect households unevenly.

In March 2026, fuel prices were still lower on a year-on-year basis, helping suppress the transport component of CPI. Within weeks, however, the April and May fuel increases fundamentally altered that picture. Those increases matter well beyond the fuel station forecourt.

Transport costs feed into food distribution, logistics, consumer goods pricing, school transport and household operating costs across the economy. The result is that many households continue experiencing rising financial pressure despite the relatively modest headline inflation number.

At the same time, salary increases across many sectors remain relatively constrained. Average salary growth in South Africa currently sits close to 5%, which means income growth is increasingly struggling to keep pace with the categories that matter most to long-term household stability. That is where the real pressure begins to emerge.

The compounding effect

A 6% increase in school fees or a 7% increase in medical aid premiums rarely feels catastrophic in a single year. Most households absorb these adjustments incrementally, often through smaller lifestyle trade-offs rather than dramatic financial decisions.

Over longer periods, however, the mathematics becomes considerably more demanding. At 6%, school fees increase by roughly 80% over a decade and more than double over a typical 12-year schooling cycle. Medical aid follows a similar trajectory over time, while fuel, transport and municipal charges continue introducing periodic shocks into household budgets.

These increases accumulate gradually rather than dramatically. The pressure rarely arrives all at once. Instead, it compounds quietly over years, steadily claiming a larger share of future income.

Structural household costs continue to rise faster than income growth for many South African households.

10-Year cumulative percentage increases compared with inflation

Why this matters from a planning perspective

Understanding the relationship between various costs of living and the benchmark Consumer Price Index (CPI) directly affects the nature of financial planning. For many investors, the central question increasingly revolves around the sustainability of future lifestyle commitments relative to long-term income growth. Schooling costs, healthcare inflation, housing expenses and retirement planning all interact over extended periods, particularly within an environment of relatively constrained wage growth and subdued economic expansion.

That places greater emphasis on integrated financial planning rather than isolated product decisions. Traditional financial planning focuses heavily on conventional investment products (retirement annuities, unit trusts, insurance structures, etc.). Seldom is the dimension of inflation differentials considered in this fairly simplistic planning.

Modern financial planning increasingly requires something broader and more dynamic, particularly where structural lifestyle inflation becomes a long-term consideration.

Editors note: This is precisely where GTC’s TrueNorth platform becomes particularly relevant.

The bottom line

South African CPI may(?) finally be behaving in a more predictable manner, but many of the costs shaping long-term household finances continue to rise steadily above CPI.

South African CPI may(?) finally be behaving in a more predictable manner, but many of the costs shaping long-term household finances continue to rise steadily above CPI.

School fees, medical aid and other structural lifestyle expenses increasingly demand a larger share of household income over time, particularly within an environment where salary growth remains constrained and fuel-related pressures continue filtering through the broader economy.

For households navigating these pressures, the challenge increasingly lies in understanding how future income, inflation and long-term commitments interact over extended periods. That process requires more than budgeting. It requires integrated planning, realistic modelling and the ability to test long-term financial sustainability before pressure becomes visible in day-to-day cash flow.

Adaptability and the ongoing understanding of one’s investment portfolio relative to the prevailing factors that influence this, is perhaps the main call-to-action regarding this topic.