Market Overview – First quarter 2026

Market commentary

The economic fallout from the third Gulf war – involving the United States, Israel, and Iran – has severely restricted supply from one of the world’s most significant oil producing regions. This has created a fear fueled environment which has caused investors around the globe to divest from ‘risk-on’ assets like equities (shares), emerging market assets, and emerging market currencies in favour of ‘safe haven’ assets such as the dollar and US government bonds over the month of March. The view of the quarter is considerably less discouraging and reminds us that short term periods of uncertainty are far less impactful over the longer term.

-

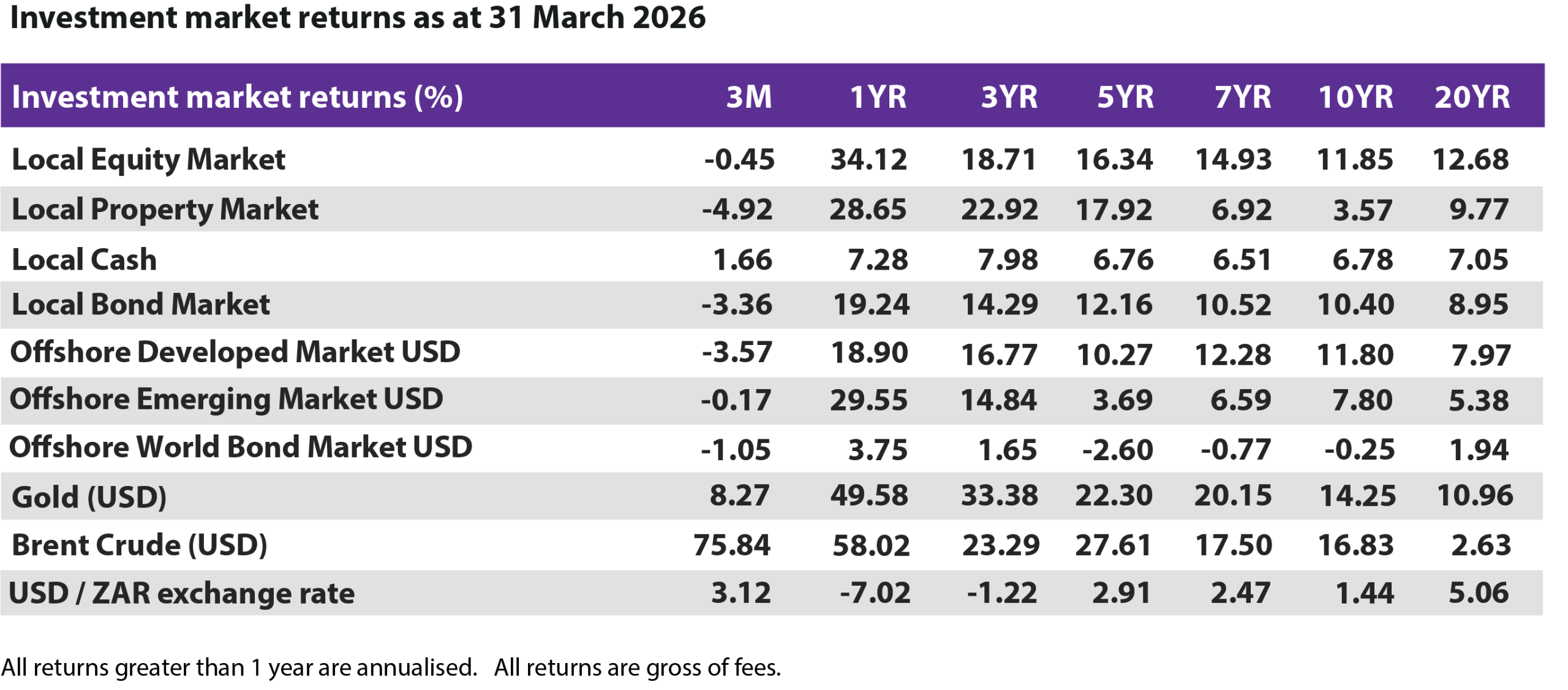

Local Growth Assets: During March, the broad-based local equity market (-10.6%) reversed gains earned in January and February to end the quarter down -0.5% amid the ongoing Gulf war. Despite a -16.5% return in March 2026, the Resources sector gained +7.2% over the quarter. This was supported by notable gains from Sasol (+112.2%) and Glencore (+40.4%). The Financials sector declined -0.3%, the Industrials sector -8.4% and the local property sector -4.9% for the quarter.

-

Local defensive assets: Amidst pre-war expectations of interest rate cuts and post-war expectations of interest rates hikes, global bond yield volatility increased over the quarter. The local bond market declined -3.4% over the quarter, lagging local cash which earned +1.7%.

The local bond market declined -6.7% over the month of March compared the +0.6% earned by local cash. The South African Reserve Bank (SARB) kept the repo rate at 6.75% in their March 2026 meeting given inflation risks from elevated energy prices amid the Gulf war. South Africa’s removal from the Financial Action Task Force (FATF) ‘grey list continues to lift investor sentiment and supported foreign inflows over the past few months.

-

Global rate cuts: In March 2026 the US Federal Reserve kept interest rates unchanged within a range of 3.5% to 3.75. The European Central Bank (ECB) also kept their rates unchanged following its March 2026 meeting. China’s annual inflation rate increased to 1.3% in February 2026, rising from 0.2% recorded in January 2026. China’s central bank kept its key lending rates unchanged for a tenth consecutive month in March 2026 as anticipated by the investors. The conflict in the Middle East has resulted in disrupted energy supply chains and contributed to inflation concerns across the globe.

-

Offshore Developed Equity Markets: The MSCI World Index declined -6.4% for the month of March and -3.6% USD for the quarter. Energy stocks gained over the quarter as the producers, refiners, and energy infrastructure companies all benefited from higher oil prices. After factoring in the USD strength, the return increased to +0.4% in rands over the quarter.

-

Offshore Emerging Equity Markets: The MSCI Emerging Markets Index retracted -13.1% over the month of March and -0.2% USD for the quarter, outperforming its developed market counterpart. South Korea and Taiwan continued to lead in the Emerging Market index for January and February supported by a weaker dollar and ongoing strength in artificial intelligence (AI)-related technologies.

They however, experienced a reversal in March as high energy costs and supply chain disruptions weighed on global sentiment. China’s anti-involution policy which aims to restore profitability, improve product quality, and manage overcapacity continued to positively impacted market sentiment as well.

-

Exchange rate and commodities: The USD relative to the rand whipsawed though the quarter ranging between R15.60 and R17.20, ending the quarter at R16.90. This represents a USD weakening +7.0% relative to the rand over the month of March and -3.1% for the quarter amidst the onset of the Gulf war. Gold continued its upward rally at the start of the year, peaking at $5562 in February, retreating some -11.2% during March 2026, closing at $4675/oz.

Amidst the closure of the Strait of Hormuz, Brent Crude surged 43.8% over the month and 75.8% over the quarter, closing at $118/barrel. Directly affecting consumers, this led to an initial petrol and diesel price recovery increase of R3.1/litre and R7.4/litre – inclusive of a R3.0/litre temporary government reduction in the general fuel levy.

GTC’s portfolios remains well-positioned to protect capital in an environment of elevated market volatility, global uncertainty and escalating geopolitical tension. While we anticipate volatility to remain in the market for the short term, our outlook for South African assets – as well as certain international markets – remains positive over the medium to longer term given current valuations and growth drivers over this period.

GTC is therefore maintaining a cautiously optimistic approach to portfolio positioning as we navigate the current market environment.

While the long-term ramifications of this Gulf war remain uncertain, we believe that maintaining a disciplined, long-term investment horizon and a well-diversified portfolio is crucial.

For all our clients, we recommend maintaining investing in line with your originally identified risk and return objectives.