Market Overview – Third quarter 2024

In-depth market commentary – Stay the course, patience pays off

In previous market commentaries, we have spoken of the old adage ‘it’s not about timing the market but rather the time in the market that matters’. This past quarter re-affirmed this message. Whilst a myriad of global factors continues to threaten a further protracted economic and investment market recovery, investors who have exited the market (in their pursuit of timing it) would have been denied the meaningful investment return bounce over the past quarter.

Over the quarter:

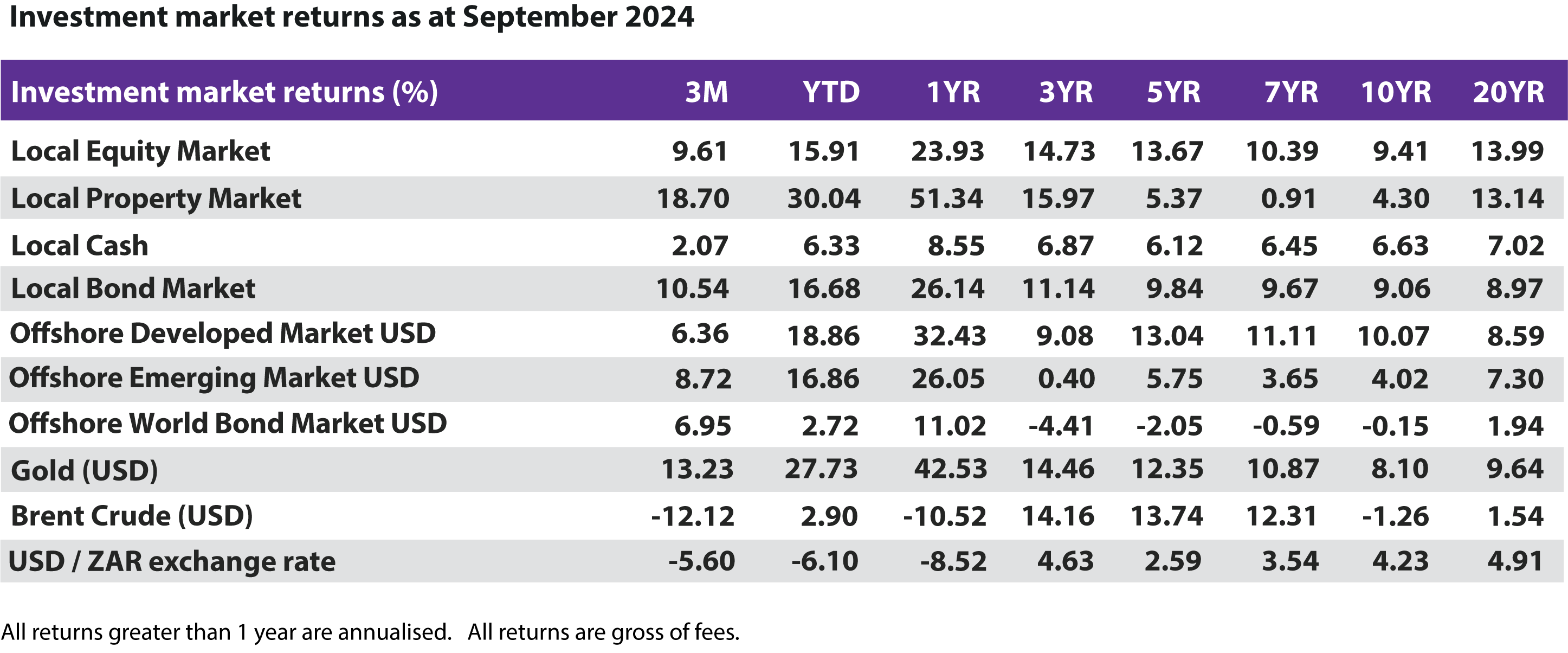

- Local equities ended the quarter up +9.6%, well ahead of Developed Market Equity and Emerging Market Equity indices in base currencies. The month of September alone reported a +4.0% gain as investor sentiment turned positive on the back of global and local monetary stimulus.

- The local Listed Property sector led the way with an +18.7% rally followed by a +13.9% bounce in the Financials sector and +11.6% in the Industrials sector. While subdued global commodity prices rebounded in September, the listed Resources sector still ended the quarter in the red, down -1.1%.

- Improved global growth sentiment spurred a rally in bond purchases from both local and foreign investors, propelling the local bond market (+10.5%) to outperform local equites over the quarter and come in ahead of local cash (+2.1%). The South African Reserve Bank (SARB) cut interest rates 0.25% to +8.0% over the quarter as headline inflation (CPI) cooled down to +4.4%.

- In September, the US Federal Reserve exceeded market expectations by cutting interest rates by half a percent to 5.0%, instead of the anticipated quarter of a percent. Fed Chair Jerome Powell stated that overall, the US economy remains strong and that such strength will allow the central bank to continue decreasing rates over time. The European Central Bank lowered its key deposit rate by +0.25% for the second time, in line with market expectations, while the Bank of England held its key rate steady at +5% during its September 2024 meeting

- China’s unprecedented stimulus package announced in September led to market optimism about forthcoming global growth and pushed the MSCI Emerging Markets Equity index up +8.7%, ahead of the MSCI World Equity Index at +6.4% for the quarter in USD.

- The price of Gold ended the quarter $2634 an ounce, up 13.2% amid continued demand for the commodity by central banks seeking to de-dollarise, as well as by safe-haven asset seekers. Subdued global demand prospects along with increased global supply pulled the price of Brent Crude oil down -12.1% over the quarter. The greenback (US Dollar) continued to weaken against the rand over the quarter some -5.6%, detracting from rand-denominated offshore market returns.

- Overall, global investor sentiment was mixed over the quarter. While the short-term outlook is still unclear, the longer-term picture remains positive.

GTC remains cautiously optimistic about the future-outlook of investment markets. We reiterate our stance that patience, especially through periods of difficult investment performances, afford markets the time needed to filter out what is relevant from the noise. It allows market drivers the required time to achieve a new state of normalcy and portfolios the time needed to compound growth on growth.

Though the investment road may be bumpy, GTC has designed its solutions to hedge out much of the inherent investment risk while still positioning the portfolio for the highest probability of delivering on its investment objectives. It is crucial to stay invested in line with one’s investment objectives when trying to achieve one’s financial goals, and not be swayed by short-term sentiment.

(These last two paragraphs are a repeat from last-quarter’s report, though GTC believes these to be as important, or perhaps even more so, than last quarter. Accordingly, no apology is given for this repetition).