Market Overview – Third quarter 2023

In-depth market commentary – Staying focussed on the long-term goal

The quarter ending September 2023 has continued to reflect a challenging global investment market backdrop. Enduring economic uncertainty has prolonged elevated investment market volatility. Subdued global trade and stubborn core inflation has led to persistently restrictive monetary policies from global central banks which with the elevated yields have kept markets on an uneven footing. As previously communicated, heightened risk factors necessitate continued caution in portfolio positioning.

Over the quarter:

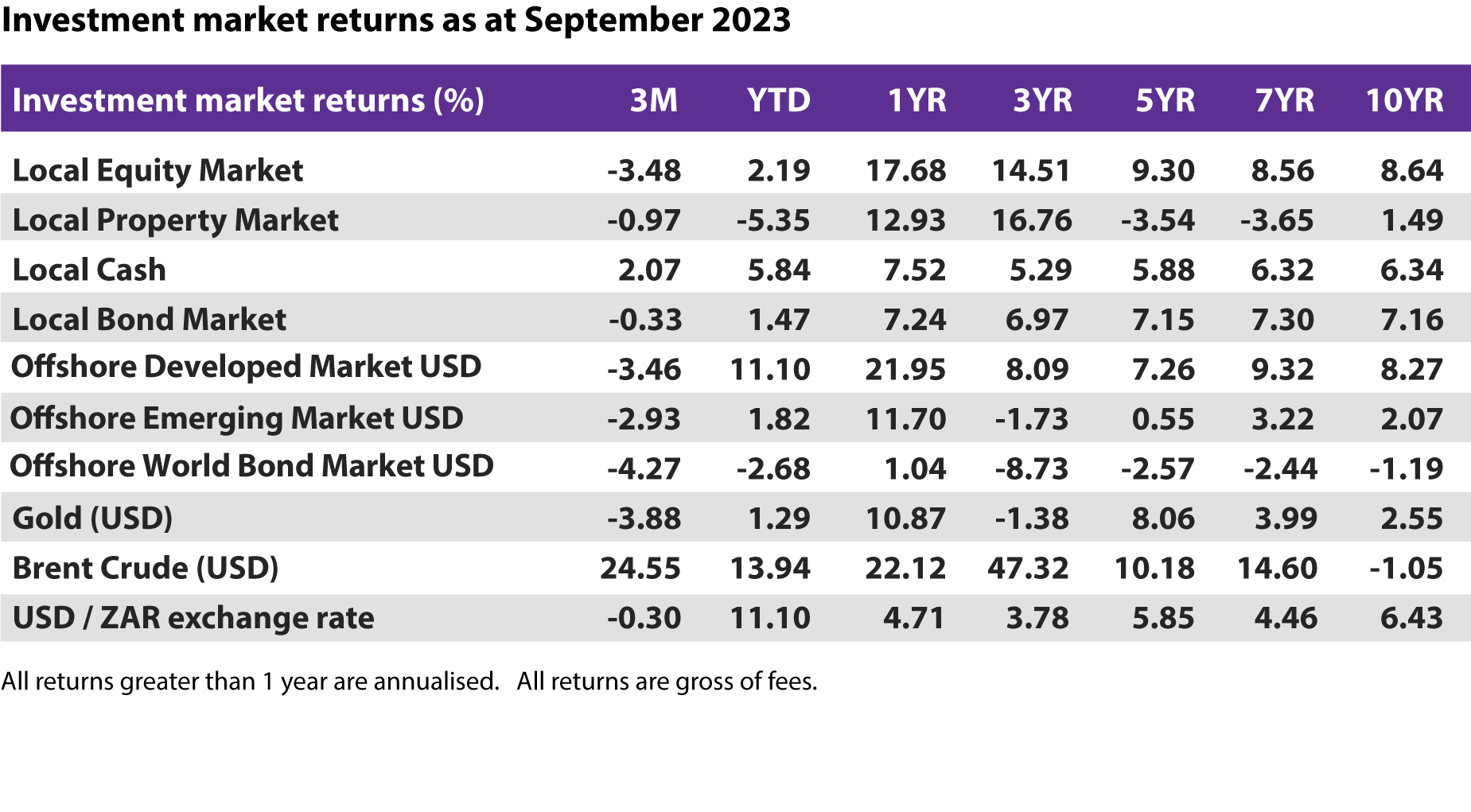

- Much of the tumultuous investment market environment this year has been masked by the share price gain of a few global technology companies primarily linked to the artificial intelligence space. These shares represent a large weighting within global developed market indices and almost fully account for the entirety of the positive dollar-based performance delivered by the S&P500 index (US equity market) over these nine months. While the collection of these few stocks has retreated over the past quarter, their impact has kept the developed market index return above +10% USD for the year. It is important to remember that while strong returns can be generated from a concentrated source, it does come with significant risk of capital loss as evidenced by the -40% loss experienced by these same few stocks in 2022.

- Global developed market equities detracted -3.5%, behind emerging market equities of -2.9% in dollar terms. The dollar weakened -0.3% relative to the rand, further detracting from offshore assets’ rand-based return.

- Negative global investor sentiment resulted in a detraction to the local equity market return over both August and September and has pulled the quarter’s performance into the red. This was primarily attributed to a decline in the local industrials sector (-6.2%) and local resource sector (-5.4%) amid global trade uncertainty and softer precious metal prices. The local property sector contracted -1.0% while the financials sector gained nearly +2.0%.

- The South African Reserve Bank (SARB) kept interest rates unchanged at +8.25%. This represents an overall +1.25% interest rate hike since the start of 2023 in their efforts to reduce inflation.

- South African headline inflation (CPI) peaked in July 2022 at +7.8% and slowed to +4.8% in August 2023, a level well within the SARB’s target range (3% – 6%). While this is a comfort, it by no means dissolves inflation concerns as global trade and energy challenges remain a headwind.

- On a similar note, US headline inflation came in at +3.7% for the year ended August 2023 while the European Central Bank (ECB) saw a meaningful decline in inflation from +5.5% at the start of the quarter to +4.3% at the end. In response to above-target-rate inflation, the US FED hiked interest rates by 0.25% to 5.5% over the quarter while the ECB increased rates by a total of 0.5% to +4.5%.

- The local bond market (ALBI) delivered -0.3% for the quarter behind local cash (STEFI) at +2.1%. The Global Government Bond Index (WIGBI) experienced a -4.3% decline over the quarter as yields pushed up amid market fears.

- The US government debt level has ballooned close to its allowed debt limit, resulting in market fears of a US government shutdown and potential default. To avert this, congress passed a stopgap bill that affords them 45 days (until 17 November) to agree on a final budget and conclude a bill that will further increase the debt ceiling. Failing to do so could have dire consequences.

- Overall, global investor sentiment was mixed over the quarter. While the short-term outlook is still unclear, the longer-term picture remains positive.

The global investment market environment has been volatile over the past few years. However, patience, especially through periods of difficult investment performances, affords markets the time needed to filter out what is relevant from the noise. It allows market drivers the required time to achieve a new state of normalcy and portfolios the time needed to compound growth on growth.

Though the investment road may be bumpy, GTC has designed its solutions to hedge out much of the inherent investment risk while still positioning the portfolio for the highest probability of delivering on its investment objectives. It is crucial to stay invested in line with one’s investment objectives when trying to achieve one’s financial goals, and not be swayed by short-term sentiment.